The 2021 Power Plan is the first to include a detailed analysis of the regional transportation sector.

The 7 key findings from the work, assuming continued, business as usual growth in the transportation sector:

- Electric passenger cars and light duty trucks are expected to grab market share from gasoline powered counterparts at a decent rate

- Today, demand from electric vehicles is limited, but by 2040, the annual electricity demand from electric vehicles will likely range between 1,000 aMW to 4,000 aMW

- Smart charging of cars, trucks and buses will be important to keep demand from being excessive at traditional system peak load hours in the late afternoon and early evening

- High electrification of passenger cars and light duty trucks can be expected to level-off the trajectory of roadway transportation sector emissions over time – but does not significantly lower overall emissions

- To really lower overall transportation emissions, heavy duty vehicles such as freight truck fleets must wean itself off diesel and move to alternative technologies and fuels

- Hydrogen fuel cell technology may offer a path to replace petroleum-based fuels for heavy duty vehicles, but the infrastructure is a nascent stage.

- A buildout of electrolysis hydrogen production facilities could result in consequential demand growth in the region

This section provides a high-level summary of the findings from the three modeling cases that were developed for the plan. The results shown are for the region as a whole. For a more detailed look at each individual case, see the following sections

A workbook with the summary results data is also available here: TPT_ModelResults_Summary.xls

The following two tables summarizes the transportation categories and case studies. Please refer to the transportation model page for more background on the modeling.

Roadway Transportation Mode Categories

| Category Name | Description |

| LDV | Light duty vehicles such as passenger cars, mini vans, sport utility vans, and small pickup trucks |

| HDV* | Heavy duty trucks, from Class 2 on up |

| Bus | Transit and School |

*Note that the HDV category is the combined HDV Light, Medium and Heavy categories – these are broken out in detail in each case section.

Transportation Study Cases

| Economic Growth | Case | Description |

| Power Plan reference case – economic growth drivers and travel and freight requirements remain consistent across cases | Reference | Forecasts a gradual shift to plug-in electric vehicles in the LDV category over the planning horizon. HDV remains primarily in diesel fuel. Direct electric vehicle options are only in the LDV and Bus categories |

| High Electric | Builds on the Reference Case but with an aggressive move to plug-in electric vehicles in the LDV category, additional electrification of transit buses, and the addition of electric trucks in the HDV Light category. | |

| H2E | Expansion of the High Electric Case with a transition to hydrogen fuel cell vehicles in the HDV Med and Heavy categories – this is considered indirect electrification |

A basic forecast of the future travel requirements for each category was developed and kept consistent across each of the three cases. The average annual rate of growth across the planning horizon for each category in terms of vehicle miles traveled, or in the HDV category, vehicle ton-miles traveled, are show in the next figure. It’s expected that the HDV category will be a key driver in terms of energy use.

Average Annual Growth Rates for Vehicle Miles Traveled from 2020 to 2045

Electric Vehicles and Demand

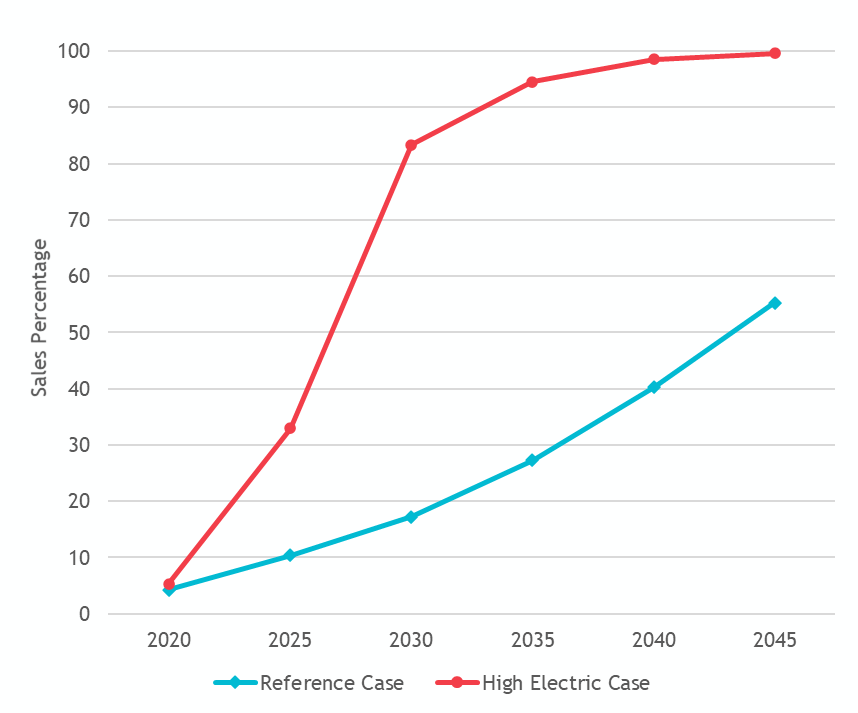

In the Reference Case, electric vehicle sales in the LDV space begin with a limited share and gradually build to nearly 60% of vehicle sales by 2045. The High Electric Case models a much quicker move to electric, led by sales in the states of Washington and Oregon. Note that the H2E Case follows the same electric vehicle sales path as the High Electric Case.

Market Share of Electric Vehicle Sales in LDV Category

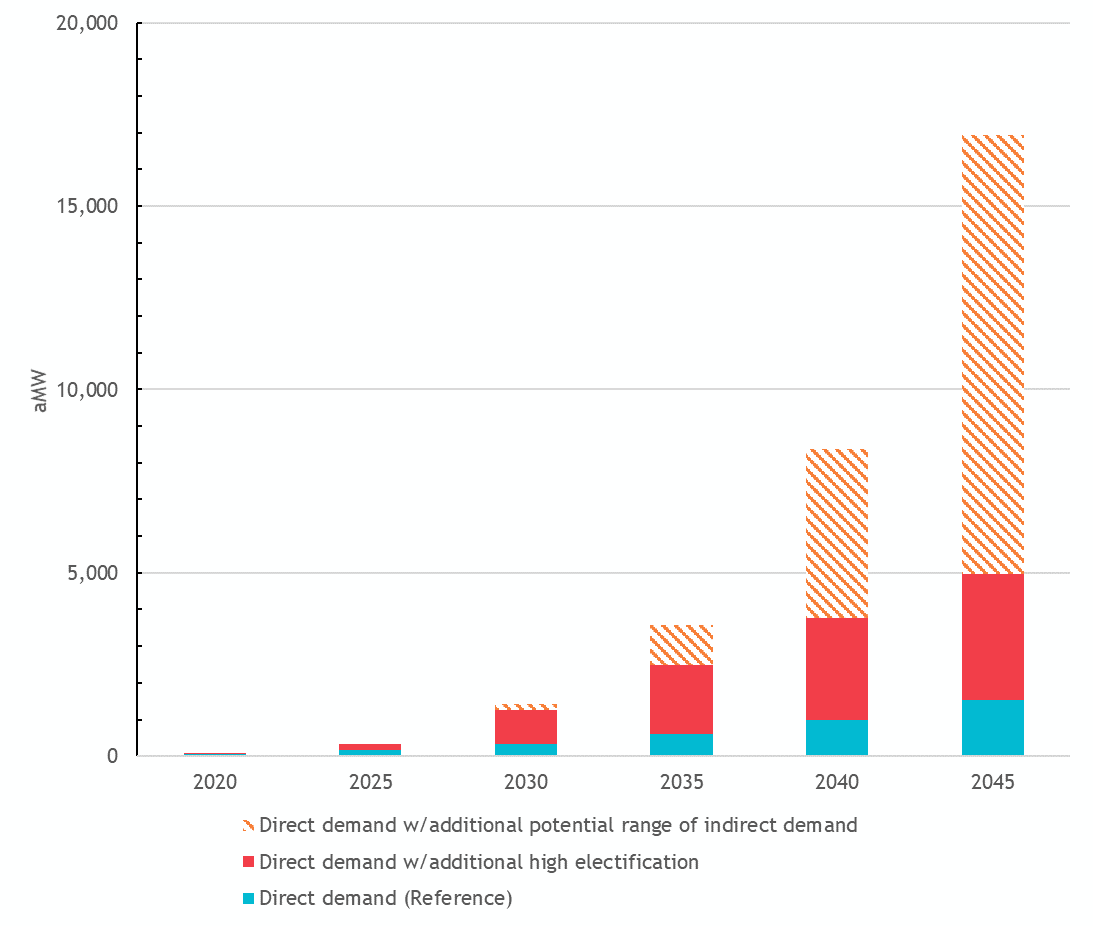

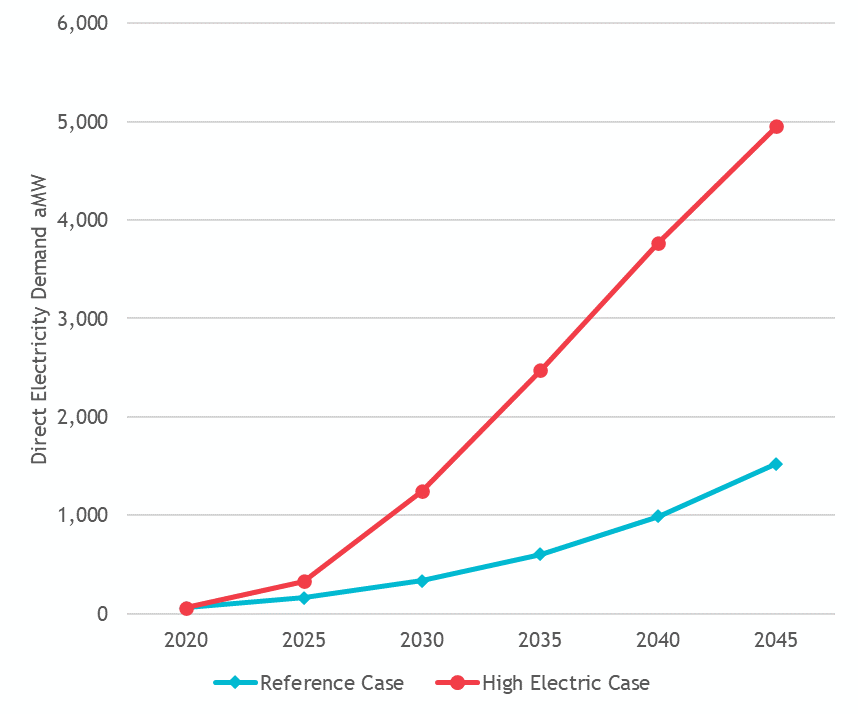

The demand for direct electricity – the electricity required for plug-in battery electric cars, trucks and buses – grows gradually in the Reference Case. Nearly all of the demand for electricity comes from cars and light trucks - the LDV category - but there is some limited demand coming from HDV light trucks and buses as well.

With a more aggressive electrification future, new demand from transportation surpasses 1000 aMW by 2030.

Annual Demand for Electricity in Average Megawatts for Roadway Transportation

Fuel Demand & Emissions

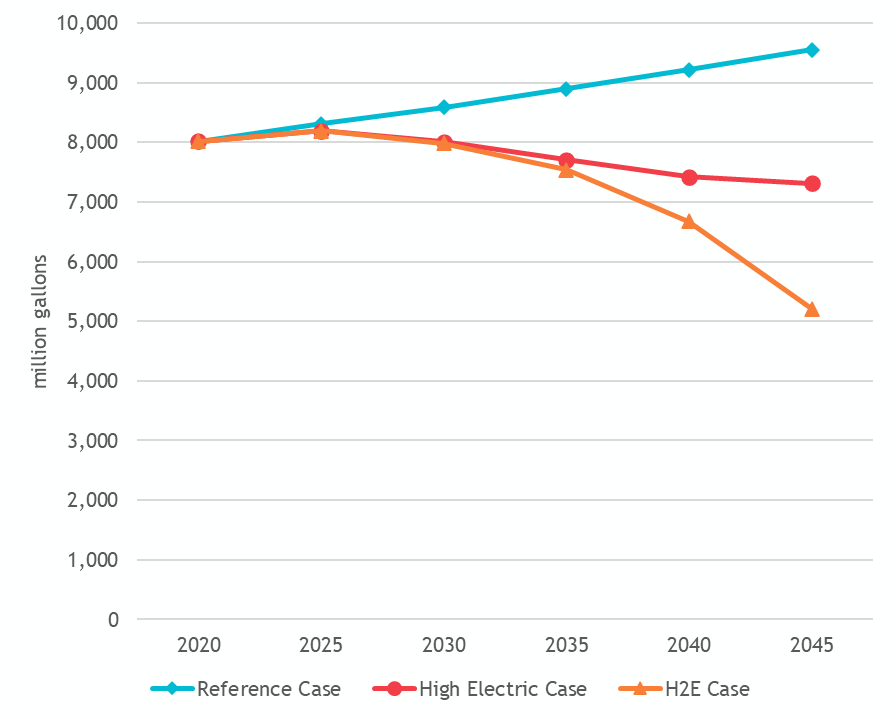

The next figure displays the petroleum-based fuel consumption for each of the study cases – this includes roadway gasoline and diesel. Diesel is the primary fuel used in trucking while gasoline is the primary fuel for cars and light trucks. Fuel cell technology is introduced in the H2E Case with hydrogen acting as a replacement fuel for diesel in the HDV category.

Annual Consumption of Gasoline and Diesel Fuel for Roadway Transportation

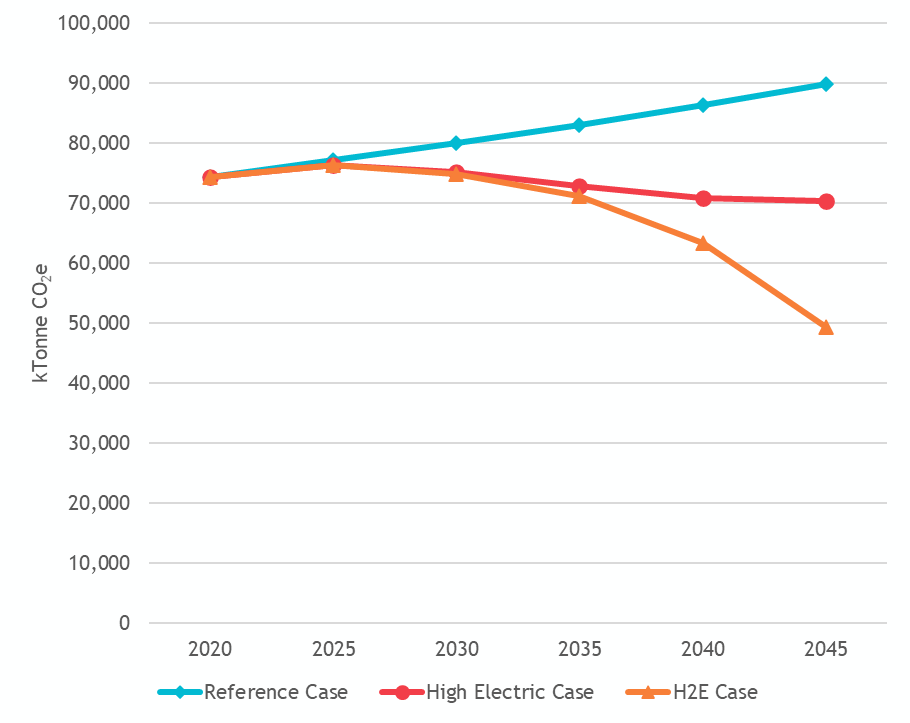

In the Reference Case, tailpipe emissions (in carbon dioxide equivalents CO2e) grow overall at an average annual rate of 0.8%. This increase occurs even as the emissions from the LDV category drop by an average annual rate of 0.6%. The issue is the heavy-duty category where there aren’t available alternative fuels options for diesel - at least not now. Emissions grow at an average annual rate of 2.9% in this category.

High electrification of cars and light trucks does bend the overall emission curve down by an annual average decline rate of 0.2%. The emission curve can be bent further by moving to hydrogen fuel cells for heavy-duty vehicles, resulting in an average annual rate of decline at 1.3%.

Annual Tailpipe Emissions from Roadway Transportation

Direct and Indirect Electricity Demand

By replacing diesel fuel in heavy-duty vehicles with fuel cells and electrifying light duty vehicles, the H2E Case results in a drop of nearly 25,000 kTonne of CO2e in terms of annual tailpipe emissions.

We discussed the impact of direct, plug-in electric vehicle demand earlier. However, for fuel cell vehicles, the hydrogen must be produced and delivered to filling stations which would in turn create new electricity demand. The following table shows the annual hydrogen demand along with an estimate of the indirect electricity that would be required to produce and prepare the product for delivery. For addition information on hydrogen see the Hydrogen & Fuel Cells page.

Annual Hydrogen Demand and Indirect Electricity Requirements from the H2E Case

| Energy | Units | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 |

| Hydrogen | KTonne | 0 | 0 | 29 | 177 | 779 | 2,185 |

| Electricity | aMW | 0 | 0 | 190 | 1,094 | 4,596 | 11,980 |

If hydrogen fuel cell vehicles did replace diesel powered heavy-duty vehicles, the addition demand for electricity could be significant. However the production of hydrogen and resulting demand for electricity would not necessarily all occur in the region. The hydrogen could be produced elsewhere and trucked in or delivered via pipeline.

The following figure displays what the outlook for the full range of potential new electricity that this limited modeling exercise indicates. The stacked column begins with the direct electricity demand from light duty vehicles from the Reference Case. Next the additional direct electric demand is added from the High Electric Case. Finally, the potential of additional indirect demand from hydrogen production is indicated with the cross-hatched block.

Range of Potential Annual Electricity Demand in Average Megawatts for Roadway Transportation